Fine wine has quietly become one of the most discussed assets in family office conversations across Australia and the APAC region, and the numbers behind that shift are striking. Family offices and wine investing are no longer a peripheral pairing. Over one-third of investors now allocate 21 to 30% of their wealth to fine wine, up from just 2% the prior year. This guide examines why that reallocation is happening, how to build and manage a fine wine portfolio with discipline, what risks demand your attention, and where the market is heading in the years ahead.

Table of Contents

- Key takeaways

- Why fine wine attracts family offices

- Building and managing a fine wine portfolio

- Risks and challenges in fine wine investing

- Emerging trends shaping wine investment

- My perspective on wine as a family office asset

- How Cellared Fine Wine supports family offices

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Wine allocations are surging | Over one-third of investors now allocate 21–30% of wealth to fine wine, reflecting a sharp rise in confidence. |

| Separation of cellars matters | Keeping investment stock apart from drinking stock protects provenance and preserves resale value. |

| Storage is a performance factor | Professional bonded warehouse storage is standard practice for high-value collections and directly affects exit pricing. |

| Transparency protects capital | Opaque pricing from wine investment companies is a material risk; clear audit trails and market-based benchmarks are non-negotiable. |

| Technology is reshaping the market | AI-driven provenance verification and real-time pricing data are improving transparency and accessibility for professional investors. |

Why fine wine attracts family offices

The appeal is not sentimental, though sentiment does play a role. Fine wine earns its place in a sophisticated portfolio for structural reasons: historical returns, market independence, and an intrinsic scarcity that no balance sheet decision can manufacture.

Returns of 6 to 10% annually are frequently cited by wealth managers, alongside the observation that fine wine carries low correlation to equity markets. When share prices contract under monetary pressure or geopolitical stress, the value of a 2005 Pétrus or a vertical of DRC Romanée-Conti does not move in sympathy. Fine wine valuation is driven by scarcity rather than earnings or energy costs, insulating it from the industrial and corporate shocks that periodically devastate traditional portfolios.

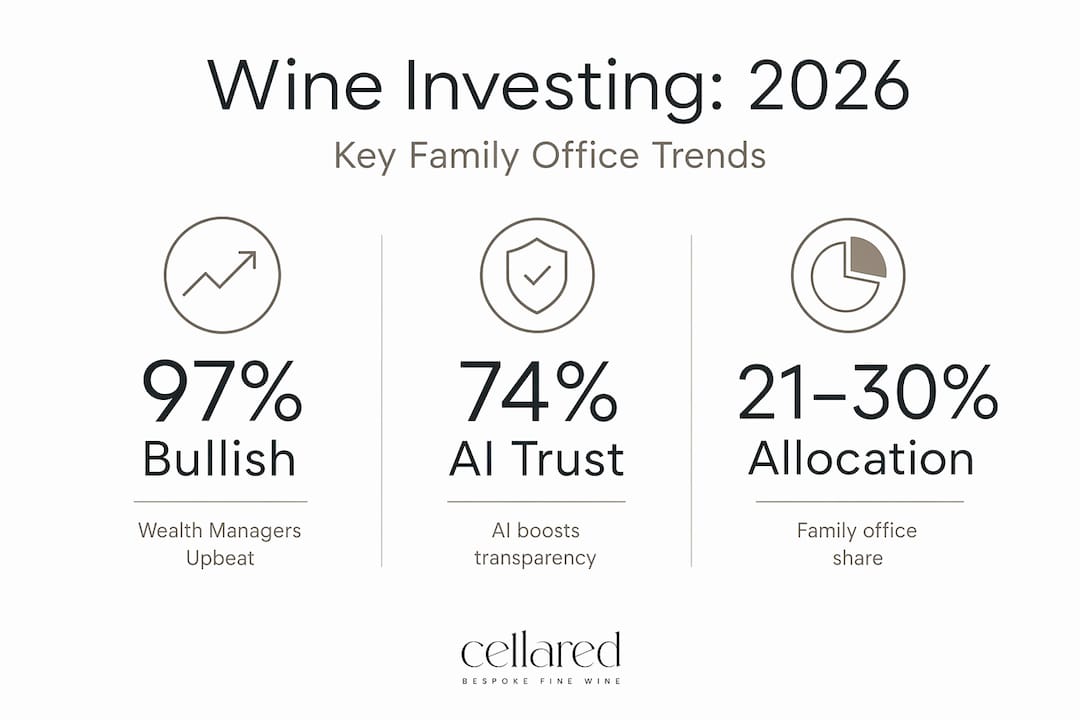

The most recent data reinforces this confidence. 97% of wealth managers are bullish on fine wine demand heading into 2026, with 71% citing stability and 57% citing strong returns as primary drivers. Those are not the numbers of a niche curiosity. They reflect a considered reclassification of wine as a core luxury asset.

Beyond the financial case, family offices are increasingly attentive to what Schroders describes as the emotional and legacy dimension of wine collections. As one perspective articulates it, wine collections form part of intergenerational wealth transfer strategies, valued not only for their market price but for the stories, provenance, and cultural weight they carry across generations. For families stewarding multigenerational wealth, that combination of financial and legacy value is genuinely rare.

Consider what distinguishes fine wine from other luxury asset classes:

- Low equity correlation. A Burgundy grand cru does not reprice when the ASX 200 drops 8% in a session.

- Inflation resilience. Physical scarcity and global demand mean wine prices tend to hold or appreciate during inflationary periods.

- Global portability. Fine wine is treated as a borderless asset class, particularly valuable for mobile high-net-worth individuals navigating shifting tax jurisdictions.

- Dual utility. Unlike gold bullion, wine can be consumed, gifted, or auctioned, giving it a lived quality that resonates with family office mandates.

"Fine wine offers something equities and bonds cannot: a tangible, scarce, globally recognised store of value that appreciates not despite time, but because of it."

Building and managing a fine wine portfolio

The distinction between a drinking cellar and an investment portfolio is one of the most consequential decisions a family office will make in this space. Conflating the two erodes returns. Blending drinking and investment stock leads to bottle opening, provenance loss, and reduced resale value. Discipline here is structural, not merely aspirational.

A well-constructed fine wine portfolio typically follows a deliberate sequence:

- Define the mandate. Clarify whether the objective is capital growth, inflation hedging, legacy building, or a combination. This shapes region selection, vintage weighting, and liquidity expectations.

- Establish an investment horizon. Typical horizons run five years, though high-growth scenarios can shorten this. Shorter horizons demand more liquid, recognised labels. Longer horizons open the door to emerging appellations and less traded producers.

- Source with provenance in mind. Every bottle's history matters. En primeur purchases direct from négociants or reputable merchants provide the cleanest provenance. Secondary market acquisitions require careful verification.

- Store in a bonded warehouse. Professional in-bond storage at facilities such as London City Bond Drakelow is standard practice among serious investors. It preserves duty-free status, maintains provenance integrity, and removes the risks of domestic temperature variation and handling.

- Diversify across regions and vintages. Concentration risk is real. A portfolio weighted entirely toward Bordeaux first growths is exposed to both appellation-specific sentiment and the preferences of a narrowing buyer pool. Burgundy, Barolo, Champagne, Rhône, and select New World producers each offer distinct risk and return profiles.

- Engage specialist advisory. Data-driven portfolio platforms and specialist advisors, rather than generalist wealth managers, are best placed to track secondary market pricing, auction results, and emerging demand trends.

Pro Tip: When building your fine wine portfolio, consider allocating a separate budget for wine intended for personal enjoyment. Keeping it entirely off the investment ledger removes the temptation to "open an investment" and protects your portfolio's provenance record.

Minimum entry points for professionally managed accounts sit around £5,000 (approximately $10,000 AUD), with average portfolios closer to £65,000 (approximately $115,000 AUD). For APAC family offices accustomed to allocating seven-figure sums across asset classes, these thresholds are modest. The real consideration is not size of entry, but rigour of process.

Risks and challenges in fine wine investing

Fine wine rewards patience and punishes carelessness. The risks are real, specific, and entirely manageable with the right framework.

- Provenance and storage failures. A bottle stored at home, or transported without temperature control, can lose a significant portion of its resale value regardless of the label. Provenance is the foundation of exit pricing.

- Mixing personal and investment stock. This bears repeating because it remains the most common mistake among first-time wine investors. Separating investment stock is not optional if capital preservation is the goal.

- Opaque pricing from wine investment companies. Some operators in the wine investment space present misleading pricing, hide markups, or fail to disclose fees in any transparent way. Professional investors prefer clear audit trails, market-based pricing benchmarks, and documented exit strategies. If a provider cannot deliver all three, look elsewhere.

- Liquidity constraints. Fine wine is not liquid in the way that equities are. Exit routes include auction houses, merchant resale, and peer-to-peer markets, each with different timelines and cost structures. Build this into your financial modelling.

- Regulatory and tax considerations. In Australia, fine wine held as an investment asset may attract capital gains tax on disposal. Wine held for personal use or consumption is treated differently. APAC jurisdictions vary considerably. Specialist tax advice, specific to wine as an asset class, is worth obtaining before committing meaningful capital.

Pro Tip: Before engaging any wine investment provider, request a full fee schedule, a sample audit trail, and at least two independently verifiable exit transactions from their book. Legitimate operators will provide all three without hesitation. For a thorough overview of the key risks in wine investing, consider reviewing specialist guidance before committing capital.

Emerging trends shaping wine investment

The fine wine market is not static, and for family offices with longer investment horizons, the technology developments now reshaping it deserve close attention.

| Trend | What it means for family offices |

|---|---|

| AI-driven provenance verification | Reduces fraud risk and increases confidence in secondary market acquisitions |

| Real-time pricing analytics | Allows portfolio managers to track market movements with greater precision and timing |

| Digital managed portfolio platforms | Enable professional wine investment without physical possession or logistical complexity |

| Accessibility for new demographics | Broader investor participation deepens liquidity and strengthens secondary market pricing |

| Cross-border wealth mobility | Fine wine's status as a borderless asset supports portfolio continuity during jurisdictional shifts |

74% of wealth managers expect AI to accelerate trust and transparency in wine markets through 2026. That is a significant signal. Historically, the opacity of wine pricing has been one of the asset class's structural weaknesses. Real-time data analytics and AI-driven verification are addressing this directly, making the case for fine wine as a professionally managed asset class considerably more credible.

The intersection with global wealth migration is equally significant. As high-net-worth individuals across the APAC region reassess domicile, tax exposure, and asset allocation, fine wine's quality as a physically portable, culturally recognised, and jurisdiction-independent store of value becomes genuinely useful. It integrates naturally with broader luxury asset diversification frameworks that include art, jewellery, and real property.

My perspective on wine as a family office asset

I have watched the conversation around fine wine investment shift considerably over the past decade, from a polite dinner table topic to a line item on serious family office balance sheets. What strikes me most is not the performance data, compelling as it is. It is the discipline gap.

Most of the families I work with understand instinctively that a 1996 Giacomo Conterno Barolo Monfortino is an asset of extraordinary quality. What they underestimate is how quickly that asset loses its investment-grade status the moment it leaves a bonded warehouse without proper documentation, or gets pulled from a mixed cellar with no audit trail. The financial and emotional dimensions of wine are both real, but they need separate management structures.

My honest counsel is this: treat fine wine as a legitimate financial asset and give it the same rigour you would apply to a property acquisition or a private equity commitment. That means independent professional advice, documented provenance, specialist storage, and a clear exit plan. The legacy dimension, the pleasure of knowing your collection exists and grows, is a genuine bonus. But it should never be a substitute for investment discipline.

The family offices I see performing best in this space are those who separate their enjoyment cellars from their estate wine planning entirely. They treat the investment portfolio with the same meticulous care as any other capital allocation. That is not joyless. It is, in fact, the approach that lets you enjoy both dimensions with genuine confidence.

— David

How Cellared Fine Wine supports family offices

For family offices in Australia and across the APAC region, Cellared Fine Wine offers the specialised depth this asset class demands. Whether you are beginning to explore fine wine as part of your luxury asset allocation or managing an established collection that requires professional structure, Cellared brings market-led expertise to every engagement. From bespoke wine buying and portfolio construction to independent valuations prepared for insurance, probate, or private advisory purposes, the service is built around the specific needs of private clients and family wealth structures. Cellared's professional cellar management service covers storage oversight, collection audits, and provenance tracking, giving family offices the clarity and control that serious wine investment requires.

FAQ

What allocation to fine wine is appropriate for family offices?

Recent data shows 45% of investors allocate 11 to 20% of their portfolio to fine wine, while over one-third now allocate 21 to 30%. The appropriate level depends on liquidity needs, investment horizon, and existing luxury asset exposure.

Why invest in wine rather than other alternative assets?

Fine wine delivers 6 to 10% annual returns historically, carries low correlation to equities, and benefits from intrinsic scarcity that is unaffected by corporate earnings or industrial conditions. It also carries emotional and legacy value absent from most alternative investments.

How do family offices manage wine investment portfolios effectively?

Professional family offices use bonded warehouse storage, maintain strict separation between drinking and investment stock, and engage specialist advisors with access to real-time secondary market data and documented provenance records.

What are the biggest risks in fine wine investing?

The primary risks are provenance loss from improper storage, opaque pricing from unscrupulous providers, liquidity constraints on exit, and the conflation of personal use stock with investment-grade bottles. Independent audit trails and specialist advisory mitigate all of these.

How does wine valuation benefit family offices specifically?

Professional wine valuations provide accurate, court-ready documentation for insurance, probate, and private advisory purposes, protecting the financial integrity of collections that often carry both significant market value and intergenerational significance.