Wine gifting and tax implications are directly connected in Australia: a bottle of fine wine given to a client or associate qualifies as a tax-deductible business expense, provided it is treated as a genuine gift rather than entertainment. The Australian Taxation Office (ATO) draws a firm line between the two categories, and crossing it unintentionally costs you the deduction. This guide explains the distinction, the recordkeeping obligations, and the practical steps to gift wine with full confidence in your tax position.

How does australian tax law treat wine gifting and tax implications?

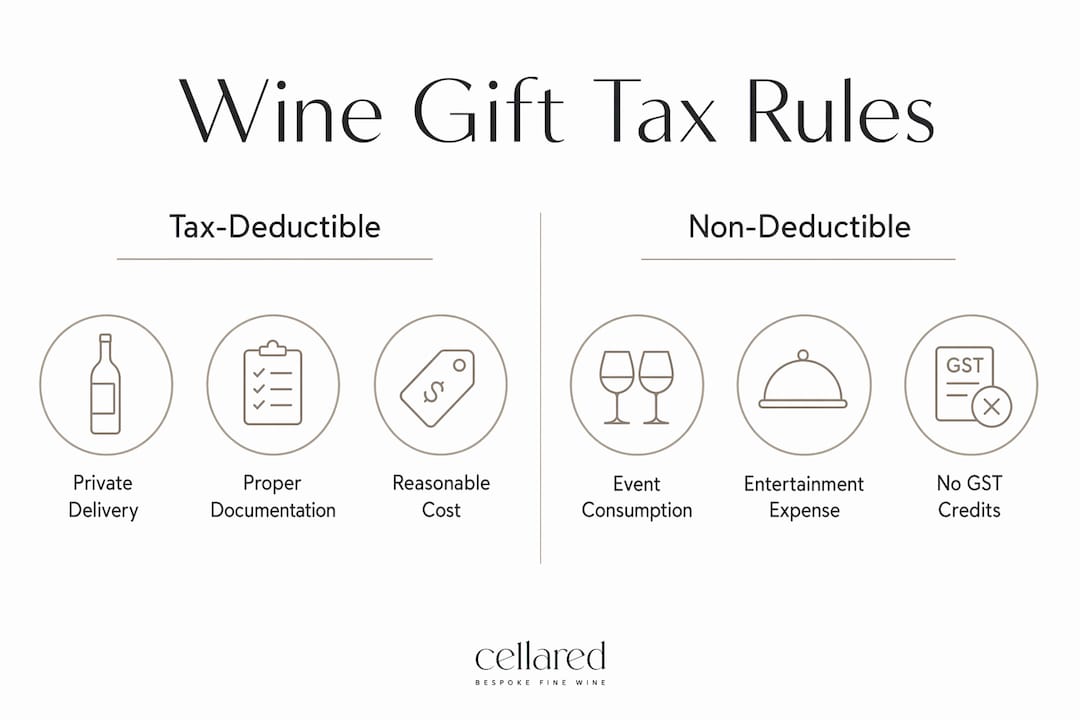

The ATO classifies wine gifts and entertainment as separate expense categories, and the difference determines whether you can claim a deduction. A wine gift is a bottle or case delivered to a recipient for their private enjoyment, with no expectation that it will be consumed in your presence or at your event. Entertainment, by contrast, covers wine served at a business lunch, a client function, or any social occasion you host.

Wine included in entertainment events is non-deductible, regardless of its quality or price. A 2021 Penfolds Grange opened at your table during a client dinner is entertainment. The same bottle couriered to that client's home the following week is a gift. The setting and the manner of consumption are what the ATO examines, not the wine itself.

Common misconceptions in this area include:

- Gifting at an event counts as a gift. It does not. Wine handed to a guest at your hosted function is still classified as entertainment.

- All client-related wine costs are deductible. Only wine given privately, outside of any hosted event, qualifies.

- Expensive wine is automatically scrutinised more. The ATO's concern is classification, not price, though excessive costs attract attention on reasonableness grounds.

- FBT applies to client gifts. FBT applies only to employee benefits, not to gifts given to clients, suppliers, or prospects.

Pro Tip: If you plan to give wine at a client event, purchase and wrap it separately from your event catering order. A distinct invoice for the gift, delivered before or after the event, keeps it clearly outside the entertainment category.

What are the recordkeeping requirements for wine gifts?

Strong, clear documentation is the cornerstone of successful tax claims related to client gifts in Australia. The ATO expects you to substantiate every deduction you claim, and wine gifts are no exception. Without proper records, even a perfectly structured gift can be disallowed during an audit.

The documentation for each wine gift should capture the following:

- Recipient's name and relationship to your business. Identify whether they are a client, supplier, referral partner, or prospect.

- Date of the gift. Record the date of purchase and, where possible, the date of delivery.

- Cost of the gift. Retain the original tax invoice or receipt showing the full purchase price including GST.

- Business purpose. Write a brief note explaining why the gift was given, for example, "thank you for the referral in March 2026" or "acknowledging a long-standing client relationship."

- Confirmation it was not consumed at a hosted event. A delivery receipt, courier confirmation, or even a brief email acknowledgement from the recipient supports this.

GST credits on wine gifts can only be claimed if the wine gift is tax-deductible under income tax rules and properly documented. This means your GST credit claim rises or falls on the same documentation that supports your income tax deduction. The two are inseparable.

Fringe Benefits Tax generally does not apply to gifts given to clients or suppliers, as these recipients are not employees under Australian tax law. If you are gifting wine to staff members, however, FBT obligations do arise, and the minor benefit exemption (currently gifts under $300 per employee) may apply depending on frequency and circumstances.

Pro Tip: Create a simple gift register in a spreadsheet or accounting software like Xero or MYOB. Log each gift at the time of purchase, not retrospectively. Reconstructed records rarely satisfy ATO scrutiny.

How much can you claim? understanding deduction limits

The cost of wine gifts must be reasonable and have a clear connection to generating assessable income to be deductible. The ATO does not publish a fixed dollar cap for client gifts, but it applies a reasonableness test. A $150 bottle of Margaret River Cabernet Sauvignon sent to a long-standing client is straightforwardly defensible. A case of 2019 Domaine de la Romanée-Conti sent to a prospect you have met once is harder to justify.

The reasonableness test considers the nature of your business relationship, the frequency of gifting, and whether the expense genuinely serves a commercial purpose. Gifting fine wine to a client who has generated significant revenue for your business is a different proposition from gifting to a cold contact.

| Scenario | Likely ATO Treatment |

|---|---|

| Single bottle to an established client, privately delivered | Deductible, GST credit claimable |

| Case of wine served at your hosted client dinner | Non-deductible, no GST credit |

| Bottle gifted to an employee at Christmas | FBT minor benefit exemption may apply under $300 |

| Wine given to a prospect with no prior relationship | Deductible if business purpose is documented clearly |

| Wine consumed at a staff party | Non-deductible entertainment expense |

Australia's approach differs from the United States, where the Internal Revenue Service caps business gift deductions at USD $25 per recipient per year. Australia has no equivalent fixed cap, which gives Australian businesses more flexibility, but also more responsibility to self-regulate on reasonableness grounds.

Practical tips for gifting wine tax-efficiently

Classifying wine costs correctly at purchase prevents misfiling as entertainment and protects your deduction claims from the outset. The practical habits you build around purchasing and delivery matter as much as the tax rules themselves.

The most effective approach to tax-efficient wine gifting combines deliberate timing, clear separation from events, and meticulous records:

- Purchase gifts on a separate invoice. Never bundle wine gifts with catering, venue hire, or event costs. A single invoice that includes both event wine and client gifts creates classification problems that are difficult to untangle later.

- Deliver gifts independently. Send wine directly to a recipient's home or office, not as a parting gesture at your hosted event. A courier receipt is your best evidence.

- Time gifts thoughtfully. End-of-year gifting in november or december is common and entirely legitimate. Gifting immediately after a significant business milestone, such as a contract signing or a major referral, is equally well-supported by business purpose.

- Avoid gifting to the same recipient too frequently. Repeated gifts to one person may attract scrutiny over whether the expense is genuinely commercial or personal in nature.

"Wine gifting is a powerful goodwill gesture, but tax efficiency depends on meeting ordinary and necessary expense criteria. Maintaining documentation of business purpose is what allows the gesture to stand up to ATO scrutiny."

Consider a practical scenario. A family-run property advisory firm in Melbourne sends a case of Yarra Valley Pinot Noir to their ten most active clients each december. They purchase the wine directly from the producer, obtain a tax invoice, log each recipient and the business relationship in their gift register, and arrange direct delivery. Each gift costs $120. The expense is deductible, the GST credit is claimable, and the records are audit-ready. The same firm also hosts a client appreciation evening in november where wine is served freely. That wine cost is non-deductible. The two expenses are kept entirely separate in their accounts, which is exactly what the ATO expects.

For families considering wine as a personal gift rather than a business gift, the tax treatment is different. Personal gifts between individuals in Australia are not subject to gift tax. Australia does not have a standalone gift tax regime. The tax implications of gifting alcohol in a purely personal context are generally nil, though if the wine forms part of an estate or a collection with significant value, other considerations such as capital gains tax on disposal may arise. The legal aspects of wine collections and their treatment under Australian law are worth understanding if you hold fine wine as an asset.

Key takeaways

Wine gifts are tax-deductible in Australia when delivered privately for the recipient's own use, properly documented, and clearly separated from entertainment expenses.

| Point | Details |

|---|---|

| Gift versus entertainment distinction | Wine consumed at your hosted event is non-deductible; wine delivered privately is deductible. |

| Documentation is non-negotiable | Record recipient, date, cost, and business purpose for every gift at the time of purchase. |

| GST credits follow deductibility | You can only claim GST credits on wine gifts that qualify as income tax deductions. |

| FBT does not apply to client gifts | FBT obligations arise only when gifting to employees, not to clients or suppliers. |

| Reasonableness governs the amount | The ATO applies a reasonableness test; gifts must connect clearly to generating assessable income. |

What i have learned about wine gifting and tax compliance

After years of working with collectors, private clients, and family estates across Australia, the single most consistent error I see is treating wine gifting as an afterthought in the accounts. A beautiful bottle of Henschke Hill of Grace is chosen with care and given with genuine warmth, yet the receipt ends up buried in a general entertainment folder, and the deduction is lost entirely.

The gift-versus-entertainment distinction is not a technicality. It reflects a genuine difference in commercial intent. A wine gift delivered to a client's door says: this is for you, at your leisure, with my compliments. Wine poured at your table says: come and enjoy this with me. The ATO recognises that difference, and so does the recipient.

My strongest advice is to review your gifting policy at the start of each financial year, not in June when the pressure is on. Decide in advance which clients you intend to gift, set a per-recipient budget that sits comfortably within a reasonableness argument, and build the documentation habit before you need it. A gift register that takes five minutes to maintain each time you purchase wine is worth far more than hours spent reconstructing records before an audit.

Fine wine is one of the most considered and lasting gifts you can give. Getting the tax treatment right does not diminish that. It simply means the gesture is as well-structured as the wine itself.

— David

How cellared fine wine supports thoughtful wine gifting

Selecting wine that is both exceptional and appropriate for the occasion requires the kind of market knowledge that goes well beyond a bottle shop visit. Cellared Fine Wine offers bespoke wine sourcing for private clients and families who want to give with genuine discernment, whether that means a single extraordinary bottle or a curated selection from a specific region or producer.

For those who hold fine wine as part of a broader collection, Cellared also provides professional wine appraisals and valuations to help you understand the market value of what you are gifting or receiving. Whether you are navigating estate planning, a family gift of significant bottles, or simply want to gift with confidence, the team at Cellared Fine Wine brings the expertise to make every selection count.

FAQ

Are wine gifts tax-deductible in australia?

Wine gifts given to clients or suppliers for private enjoyment are tax-deductible as business expenses in Australia, provided they are not consumed at a hosted event and are properly documented with recipient details, date, cost, and business purpose.

Does FBT apply to wine gifts given to clients?

FBT does not apply to wine gifts given to clients, suppliers, or prospects, as Fringe Benefits Tax only covers benefits provided to employees under Australian tax law.

Can i claim GST credits on wine i give as a gift?

You can claim GST credits on wine gifts only if the expense is income tax deductible. Wine consumed at entertainment events does not qualify for GST credits.

Is there a dollar limit on wine gift deductions in australia?

Australia has no fixed dollar cap on client gift deductions, unlike the United States. The ATO applies a reasonableness test, requiring that the cost have a clear connection to generating assessable income.

Do personal wine gifts between family members attract gift tax in australia?

Australia does not have a standalone gift tax regime, so personal wine gifts between family members are generally not taxable. However, if the wine forms part of a valuable collection, capital gains tax considerations may apply on disposal or transfer.