Fine wine collections held by high net worth individuals in Australia and across the APAC region are, by any meaningful measure, serious financial assets. Yet the legal aspects of wine collections are routinely underestimated, treated as an afterthought to the pleasure of acquisition and the anticipation of drinking. The reality is considerably more structured: licensing obligations, capital gains tax, valuation standards, bonded storage regulations, and estate planning implications all intersect in ways that can materially affect the value you preserve, transfer, or realise from a collection of genuine depth and rarity.

Table of Contents

- Understanding licensing and legal requirements for selling wine collections

- Capital gains tax and estate implications for fine wine collections

- Professional valuation and documentation of wine collections for legal security

- Bonded storage and duty deferral strategies for APAC wine investors

- Legal risks and fraud mitigation for high-value wine collections

- Why traditional estate planning often falls short for high net worth wine collectors

- How Cellared Fine Wine supports your legal and valuation needs

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Private sales licence exemption | In Australia, private wine sales at auction don’t require a liquor licence, simplifying collection liquidation. |

| Capital gains tax applies | Heirs pay CGT on inherited wine sales based on original purchase price, not date of death value. |

| Professional appraisals essential | Regular valuation by experts ensures correct estate reporting, insurance, and market alignment. |

| Use bonded storage | Bonded warehouses enable APAC investors to defer excise duties, preserving investment capital. |

| Plan with trusts | Testamentary trusts aid tax minimisation and protect wine collections from probate and mismanagement. |

Understanding licensing and legal requirements for selling wine collections

One of the most common misconceptions among private collectors is that selling wine, even at significant volume, automatically triggers complex liquor licensing obligations. The distinction matters enormously when you are contemplating divesting part of a collection, managing an estate, or advising beneficiaries on their options.

Under Australian law, no liquor licence is required for private individuals selling personal wine collections at auction. This is one of the more collector-friendly provisions in Australian liquor law, and it applies broadly across jurisdictions including New South Wales. The critical condition is that the auction must be conducted by a licensed professional auctioneer, not the collector themselves acting in a commercial capacity.

Where the legal landscape shifts is at the point of commercial activity. If you intend to sell wine regularly, operate from business premises, or trade in a way that resembles a packaged liquor retailer, a packaged liquor licence becomes necessary. In NSW, annual fees for such licences begin at approximately $816, though the compliance burden extends well beyond the fee itself. Premises requirements, record-keeping obligations, and separation of alcohol sales areas from other retail activity all form part of the regulatory picture.

For most collectors exploring liquor licence exemptions for private sales, the good news is that a thoughtfully managed auction through a reputable house sits comfortably within the non-commercial exemption. Understanding where that boundary lies protects you from inadvertent compliance breaches.

Key points to understand before selling:

- Private individuals can sell personal wine collections at auction without a liquor licence in NSW and across Australia

- Commercial sale or repeated trade in wine requires a packaged liquor licence, with annual fees from $816

- All auctions must be conducted by a licensed professional auctioneer to qualify for the private exemption

- Premises used for mixed business must maintain separate, compliant alcohol sales areas

- Non-commercial private sales to individuals, such as a private treaty arrangement, generally avoid licensing requirements entirely

Pro tip: If you are winding down a collection through multiple auction lots across different sale dates, document each transaction clearly as relating to your personal cellar rather than commercial stock. The intent and pattern of activity both bear on how regulators interpret your conduct.

With licensing clarified, let's explore how taxation, especially capital gains tax, impacts wine collections in estate planning.

Capital gains tax and estate implications for fine wine collections

Australia's approach to intergenerational wealth transfer is more nuanced than many collectors appreciate. There is no inheritance tax or estate duty in this country, which may seem to simplify matters considerably. But CGT applies on inherited wine when beneficiaries sell, and the cost base inherited from the original purchase can be decades old, meaning the capital gain on a prized Penfolds Grange collection or an exceptional Burgundy parcel may be substantial.

The mechanics work like this. When a beneficiary inherits wine and subsequently sells it, the cost base for CGT purposes is generally the original purchase price paid by the deceased, not the market value at the date of death. If that Domaine de la Romanée-Conti was acquired fifteen years ago at a fraction of its current worth, the taxable gain falls almost entirely on the heir.

"Australia has no inheritance tax or estate duty, but deceased estates trigger capital gains tax on wine collections at sale, with a 50% discount available for assets held over 12 months."

The 50% CGT discount is available where the wine was held for more than twelve months by the deceased or the beneficiary. This makes the timing of any sale a genuinely consequential decision, not merely a market-driven one.

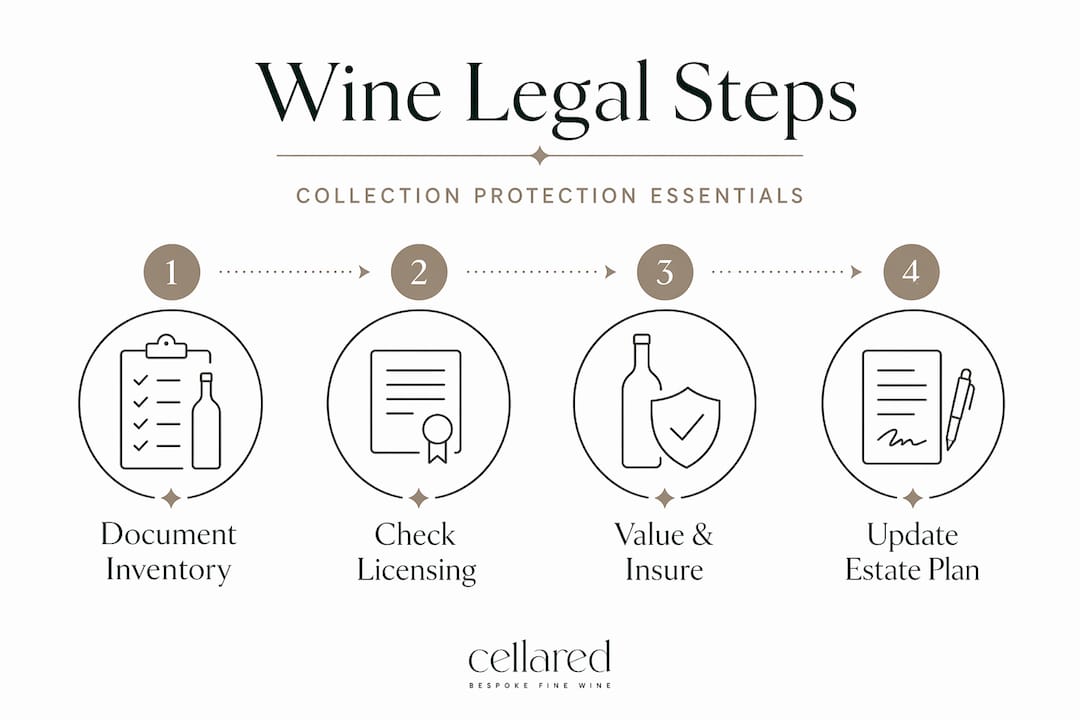

Consider these estate planning steps in sequence:

- Identify the original cost base for every significant bottle or parcel in the collection, supported by purchase receipts and auction records.

- Assess how long the collection, or individual parcels within it, has been held to determine eligibility for the 50% CGT discount.

- Review superannuation death benefit structures, as death benefits paid to non-dependants including adult children attract tax of between 17% and 32% on the taxable component.

- Consult with an estate planning adviser on the suitability of a testamentary trust, which can distribute income from the sale of wine assets flexibly across lower-income family members, reducing aggregate tax.

- Ensure your will grants executors explicit authority to manage, store, and selectively sell wine, preserving both condition and value during the administration period.

Testamentary trusts deserve particular attention here. They provide privacy, smoother estate administration, and the capacity to manage tax exposure across generations in ways that a simple will cannot match.

Understanding tax is essential, but accurate valuation underpins correct tax, insurance, and estate planning.

Professional valuation and documentation of wine collections for legal security

A collection valued at $800,000 at the time of acquisition may be worth considerably more, or considerably less, by the time it is appraised for an insurance claim, an estate, or a family law proceeding. Professional appraisals accounting for provenance, rarity, market demand, and storage conditions are not optional for collections of this magnitude. They are the documentary foundation on which every legal and financial outcome rests.

For collections valued above $500,000, bottle-by-bottle documentation is the appropriate standard. This is not excessive rigour; it is the level of specificity that courts, insurers, and tax authorities expect when a dispute or claim arises. A single-page summary valuation may suffice for a casual cellar, but it is inadequate for investment-grade wine held as a meaningful asset.

| Valuation purpose | Minimum documentation required | Review frequency |

|---|---|---|

| Insurance | Bottle-level appraisal with photos | Every 2 years |

| Probate and estate | Certified independent appraisal | At time of death |

| CGT cost base | Original purchase receipts and market comparables | At acquisition |

| Family law proceedings | Court-ready independent valuation | As required |

| Private sale or auction | Market-led appraisal with provenance notes | Prior to sale |

Proper storage condition documentation is equally important. Temperature excursions, humidity failures, or light exposure can degrade wine materially. If a collection's storage history cannot be evidenced, both insurance claims and resale values suffer accordingly.

Pro tip: Review the wine valuation checklist before commissioning an appraisal. Knowing what documentation to present, including purchase receipts, auction catalogues, and storage records, can meaningfully improve the accuracy and defensibility of the outcome.

Professional wine valuation services that align with valuation standards and best practices for 2026 are not a luxury for serious collectors. They are a prerequisite for any collection that carries genuine investment or estate significance.

With valuation foundations set, let's examine how bonded storage in APAC can defer duties and secure investment capital.

Bonded storage and duty deferral strategies for APAC wine investors

For investors holding fine wine across Singapore, Hong Kong, China, or Australia, bonded warehouse storage represents one of the most tax-efficient structures available. The principle is straightforward: wine held in a bonded facility has not technically entered the domestic market, and therefore excise duties are deferred until the wine is released for consumption or sale within that jurisdiction.

This is not a loophole. It is an established legal mechanism that has underpinned professional investment wine management for decades. The capital preserved through duty deferral can be meaningfully significant on a collection of several hundred cases of premier cru Bordeaux or aged Barolo.

From a legal standpoint, bonded storage also reinforces provenance. A continuous, documented chain of custody from négociant to bonded facility to buyer is among the strongest provenance records available. It is, in essence, an unbroken legal record of the wine's journey.

Key considerations for APAC investors using bonded storage:

- No personal liquor licence is required simply to own wine held in a bonded facility

- Import duties across jurisdictions such as Singapore and China apply only at the point of release, not during storage

- Chain-of-custody documentation generated by bonded facilities forms a defensible provenance record for insurance and resale purposes

- Investment wine held in bonded storage should remain there until sale to a buyer who will release it, preserving the duty-deferral benefit

- Bonded facilities in Singapore's FreePort and Hong Kong offer internationally recognised, climate-controlled environments specifically designed for investment-grade wine

Pro tip: When selecting a bonded facility, request written confirmation of their temperature and humidity monitoring protocols, insurance arrangements, and chain-of-custody documentation standards. The legal strength of your provenance record depends on the quality of the facility's record-keeping.

Finally, safeguarding your investment means recognising risks. We explore legal risks and fraud prevention in the wine market.

Legal risks and fraud mitigation for high-value wine collections

The fine wine market, for all its elegance and tradition, is not immune to the full spectrum of financial fraud. Wine fraud cases have surged 200% in recent months, with documented scams reaching $97 million and exploiting counterfeit provenance, forged labels, and fabricated auction histories. For collectors with holdings of genuine depth, this is not an abstract threat.

"HNWI must secure appraisals, photographs, receipts, and storage records as the primary defence against fraudulent provenance claims in insurance and estate contexts."

The legal implications extend beyond the initial loss. If fraudulent wine enters an estate and is subsequently valued and transferred to beneficiaries based on a false provenance, the downstream consequences include inflated CGT cost bases, disputed insurance claims, and potential executor liability.

Protecting your collection requires systematic attention to:

- Thorough appraisals with photographic documentation of every significant bottle, label, and capsule

- Purchase receipts and auction records retained and stored securely, ideally in digital and physical form

- Storage facility records evidencing unbroken chain of custody from acquisition to current location

- Regular expert valuation updates, particularly for bottles where secondary market prices have moved materially

- Engagement with trusted bonded storage facilities whose records would withstand legal scrutiny

The wine fraud prevention resources available to informed collectors provide a useful framework for building a fraud-resistant documentation practice. The effort invested in meticulous record-keeping is, in effect, an insurance policy within an insurance policy.

Why traditional estate planning often falls short for high net worth wine collectors

Here is the uncomfortable truth that most generalist estate planners will not tell you: a standard will, even a well-drafted one, is frequently inadequate for a fine wine collection of meaningful scale. The legal aspects of wine collections demand a level of asset-specific sophistication that generic estate planning frameworks simply were not built to provide.

The most consequential oversight we encounter is the failure to account for the original CGT cost base on inherited wine. Australian HNWI often overlook CGT on inherited wine from the original cost, and without a testamentary trust structure, adult children receiving superannuation death benefits face tax rates of 17% to 32% on the taxable component. These are not marginal issues. On a collection worth several million dollars, the tax exposure is substantial.

Testamentary trusts are not merely a tax vehicle. They provide privacy from the public probate process, offer executors and trustees structured authority to manage complex assets, and allow income from wine sales to be distributed across family members at lower marginal rates. For collections that include both investment-grade parcels and bottles intended for consumption, they also provide the flexibility to treat those categories differently in the administration.

We also observe that executors without clear, written authority and detailed instructions frequently make value-destroying decisions under time pressure. Wine left in inappropriate storage conditions during a prolonged estate administration loses condition and value. An executor who cannot distinguish a case of Penfolds Bin 707 from table wine is not equipped to manage the asset responsibly.

The hybrid appraisal approach, which clearly distinguishes investment-grade bottles from consumable ones within the same cellar, is something we advocate strongly. It allows for appropriate tax treatment, accurate insurance coverage, and estate distribution that reflects the true nature of each component. The professional valuations for estate planning that Cellared Fine Wine provides are specifically structured to deliver this level of distinction and documentary rigour.

How Cellared Fine Wine supports your legal and valuation needs

Managing the legal, tax, and valuation dimensions of a fine wine collection is, at its core, a question of having the right expertise at your side before decisions need to be made under pressure.

Cellared Fine Wine offers bespoke wine appraisals prepared to court-ready standards, reflecting provenance, rarity, storage history, and current market conditions. Our professional wine valuations are used by collectors, estate practitioners, family law solicitors, and tax advisers across Australia and the APAC region. Beyond valuation, our wine cellar management services ensure that collections are stored, documented, and maintained with the integrity that both the wines and their owners deserve. Whether you are planning an estate, preparing for a significant sale, or simply bringing rigour to a collection that has grown beyond the casual, we are here to help you act with clarity and confidence.

Frequently asked questions

Do I need a liquor licence to sell my private wine collection at auction in NSW?

No. As a private individual in NSW, you can sell your personal wine collection at auction without a liquor licence, provided the auction is conducted by a licensed professional auctioneer rather than by you in a commercial capacity.

Is there inheritance tax on wine collections in Australia?

Australia does not impose inheritance tax or estate duty, but CGT applies when heirs sell inherited wine collections, often calculated from the original purchase price paid by the deceased, which can result in a substantial taxable gain.

How often should my wine collection be professionally appraised for estate planning?

For significant collections, appraisals should be updated periodically as markets shift, with bottle-level documentation reviewed at least every two years and immediately upon any material change in collection value or composition.

Can bonded storage save me money on duties for my wine collection as an APAC investor?

Yes. Bonded storage defers excise duties until wine is released for consumption or sale, preserving capital during the investment period and providing a legally recognised provenance record across jurisdictions including Singapore and China.