A fine wine collection is more than a passion project. For high net worth collectors across Australia and APAC, it is a tangible, appreciating asset that demands the same rigorous protection as any blue-chip investment. Yet many collectors discover, only at the worst possible moment, that their standard home insurance falls well short of adequate coverage for their cellars. This guide to wine cellar insurance walks you through everything you need to know: what specialised coverage entails, how to prepare your collection, which policy structures suit which situations, and how to ensure your insurance keeps pace with your collection's growing value.

Table of Contents

- Understanding wine cellar insurance and why it matters

- Preparing your wine collection for insurance: appraisal, inventory and storage

- Choosing the right insurance coverage: blanket, scheduled or hybrid policies

- Cost considerations and common claims in wine cellar insurance

- Best practices for maintaining and updating your wine cellar insurance

- Why proactive insurance is the smartest investment in your wine cellar's future

- Protect your investment with expert wine cellar insurance and valuation services

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Specialised coverage essential | Standard home insurance rarely covers valuable wine collections adequately, making specialised insurance crucial. |

| Professional appraisal needed | Certified wine appraisals and detailed inventories are vital prerequisites for obtaining proper coverage. |

| Choose policy type wisely | Blanket coverage suits smaller collections; scheduled coverage benefits high-value and rare bottles. |

| Manage ongoing updates | Regularly update your insurance and storage conditions to maintain effective protection. |

| Proactive insurance safeguards | Rising wine values and claims highlight the importance of proactive, agreed value policies for financial security. |

Understanding wine cellar insurance and why it matters

What is wine cellar insurance, precisely? At its core, it is a specialised form of personal property coverage designed around the unique risks and values associated with fine wine collections. It is not a luxury add-on. It is a structural necessity.

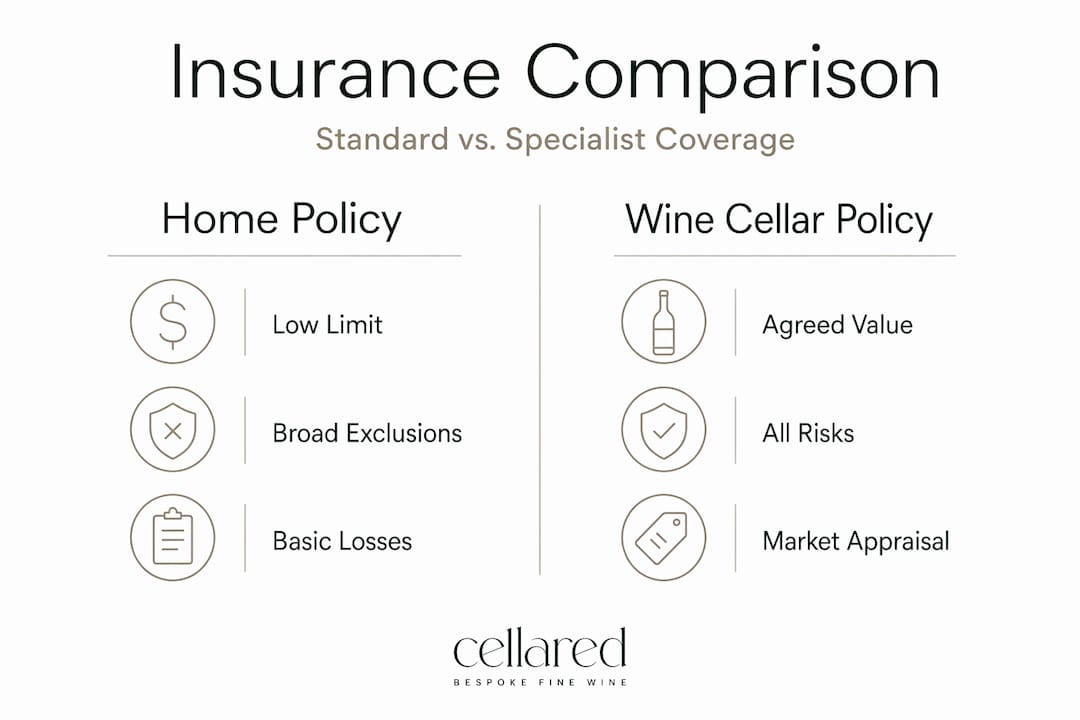

Standard home policies treat wine much like furniture or clothing: as household contents subject to a general limit and a catalogue of exclusions. Specialised policies cover theft, spoilage from temperature fluctuations, transit damage, and natural disasters in ways that a household contents rider simply cannot. The difference in coverage is not marginal. It can be the difference between a full replacement payout and receiving a fraction of your collection's true market value.

Insurance for wine cellars typically covers the following risk categories:

- Physical damage including accidental breakage during handling or storage

- Theft from the cellar, a vehicle, or a third-party storage facility

- Spoilage caused by climate control failure, power outage, or equipment malfunction

- Transit risks during transport to or from auction, a specialist retailer, or a dining event

- Natural disaster damage including flood, fire, and storm

One dimension that separates fine wine insurance from standard personal property coverage is the valuation method. Wine values fluctuate with vintage reviews, market sentiment, and auction results. An expert wine insurance guidance framework will account for this volatility by using agreed value policies rather than market value at the time of claim, which prevents painful disputes when a prized bottle's value has moved significantly since the policy was written.

| Feature | Standard home insurance | Specialised wine cellar insurance |

|---|---|---|

| Coverage limit | Low sub-limit ($1,000 to $2,500 typical) | Full collection value |

| Spoilage from temperature | Generally excluded | Covered |

| Transit coverage | Minimal or absent | Included |

| Valuation method | Actual cash value | Agreed value |

| Theft outside the home | Rarely covered | Covered |

| Per-bottle caps | Often apply | Removed with scheduled coverage |

Preparing your wine collection for insurance: appraisal, inventory and storage

Before securing insurance, it is vital to prepare your collection properly through appraisal, inventory, and storage compliance. Underwriters are precise in their requirements, and gaps in documentation can become very costly at claim time.

Here is how to prepare methodically:

- Commission a professional appraisal. For collections of meaningful value, insurers require an independent, documented assessment by a qualified expert. Wine appraisal and valuation services establish a defensible, market-led figure for each bottle, which forms the basis of your agreed value policy.

- Build a thorough inventory. Every bottle should be recorded with its producer, appellation, vintage, quantity, purchase price, current market value, and storage location.

- Photograph and document provenance. High-resolution images of labels, capsules, and fill levels, paired with purchase receipts, auction records, and certificates of authenticity, are essential for both insurers and potential future claims.

- Verify your storage environment. Most insurers require climate-controlled conditions at approximately 13°C (55°F) and 65 to 75% relative humidity, with backup power systems and robust security.

- Update regularly. A static inventory is a liability. As you acquire new bottles or your collection's value shifts, your documentation must keep pace.

Underwriters require detailed inventories, appraisals, provenance, climate controls, and security details for wine collections, and agreed value policies prevent disputes at claim time. This is not bureaucracy for its own sake. Each requirement protects you as much as the insurer.

The wine valuation checklist framework is worth consulting before you approach an underwriter. It ensures no detail is overlooked, which is precisely what distinguishes a smooth claim from a contested one.

Pro Tip: Store digital copies of your inventory, appraisal reports, and provenance documentation in a secure cloud environment, separate from the physical cellar. If fire or flood destroys the cellar, your records survive intact and your claim proceeds without delay.

- Photograph each section of the cellar, not just individual bottles

- Record serial numbers or unique identifiers for exceptionally rare bottles

- Note the name and credentials of the appraiser on all documentation

- Keep a log of any repairs or upgrades to your climate control system

Choosing the right insurance coverage: blanket, scheduled or hybrid policies

With your collection prepared, the next decision is which policy structure fits your situation. The three principal options each carry distinct advantages depending on your collection's composition, value, and rate of growth.

Blanket coverage insures the entire collection under a single limit, with per-bottle caps applied. It suits collectors with a broadly consistent range of bottles where no single item is extraordinarily more valuable than the rest. Administration is simpler, and premiums tend to be lower, but the per-bottle cap can leave rare bottles underinsured.

Scheduled coverage itemises every bottle individually with a declared value for each. This removes per-bottle limits entirely and provides granular protection for rare vintages, large-format bottles, or wines from trophy producers. For collections over $50,000 or containing rare or vintage bottles, scheduled insurance with itemised bottles over $500 is recommended, while blanket coverage suits smaller collections.

Hybrid policies combine both approaches: a blanket limit covers the general cellar population, while a scheduled rider is applied to named, high-value bottles. This is increasingly the preferred structure for sophisticated collectors whose cellars contain both everyday drinking wine and irreplaceable trophy bottles.

| Policy type | Best suited for | Per-bottle cap | Claim complexity | Typical premium |

|---|---|---|---|---|

| Blanket | Smaller or uniform collections | Yes | Lower | Lower |

| Scheduled | High-value, rare, or large-format bottles | No | Higher | Higher |

| Hybrid | Mixed collections with trophy bottles | Partial | Moderate | Moderate |

- Review your cellar composition annually. A blanket policy that was appropriate two years ago may leave gaps as your collection matures.

- Check whether your policy covers bottles stored at third-party facilities, not just your home cellar.

- Confirm that transit is included, particularly if you regularly send bottles to auction or dining events.

The approach of protecting and growing your wine collection's value is inseparable from choosing the correct policy structure. The finest bottle in your cellar deserves the finest protection designed for it specifically.

Pro Tip: When negotiating a hybrid policy, provide your insurer with a tiered inventory: bottles under a set threshold covered under the blanket limit, bottles above it individually scheduled. This keeps your premium proportionate while ensuring your most significant assets are never exposed to a per-bottle cap.

Cost considerations and common claims in wine cellar insurance

Understanding policy options naturally leads into the costs involved and common scenarios to prepare for. The cost of wine cellar insurance is considerably more approachable than many collectors expect, particularly when weighed against the asset values at stake.

Wine insurance premiums typically range from 40 to 80 cents annually per $100 of collection value. For a collection valued at $200,000 AUD, that translates to an annual premium of roughly $800 to $1,600. Against the potential loss of a single case of first-growth Bordeaux or a vertical of Penfolds Grange, this figure is rather modest.

Premiums are influenced by several factors:

- Total insured value of the collection

- Storage environment quality, including climate control and backup systems

- Security measures such as monitored alarms and controlled access

- Coverage type: scheduled policies carry higher premiums than blanket

- Claims history of the policyholder

- Location and building type of the storage facility

The most common claims in insurance for wine collectors fall into the following categories:

- Theft, particularly from residential cellars or during transit

- Spoilage from climate control failure, including power outages that allow temperature to spike

- Accidental breakage during handling, moving, or cellar reorganisation

- Water and flood damage to bottles, labels, and storage furniture

- Transit damage during auction consignment or interstate transport

"Average wine collection claims surged 238% from 2022 to 2025, rising from £4,133 to £13,966, while 50% of collectors remain entirely uninsured, exposing themselves to catastrophic financial loss."

Underinsurance is the most insidious risk in this space. Many collectors set their insured value at purchase price rather than current market value, a distinction that proves devastating when a collection has appreciated significantly. Maintaining up-to-date valuations is not an administrative nicety. It is the foundation of private client wine insurance done correctly.

Best practices for maintaining and updating your wine cellar insurance

Finally, maintaining effective insurance is an ongoing process that requires diligent management and updates. Securing a policy is not the conclusion. It is the beginning of an active stewardship relationship.

Regularly review and update your insurance as your collection grows or changes, and maintain proper climate control and security to meet ongoing policy conditions. Insurers may conduct periodic reviews and a lapse in documented compliance can create grounds for claim rejection.

- Notify your insurer of every significant acquisition, ideally within 30 days of purchase, to bring new bottles within coverage immediately

- Document all climate control maintenance, including servicing records for cooling units and backup power systems

- Review your agreed values annually, particularly for wines that have seen significant auction results or critical re-evaluation

- Understand your exclusions thoroughly, as gaps in knowledge at claim time are extraordinarily costly

- Engage your wine adviser before major acquisitions to ensure new bottles are appropriately valued and included in your policy from day one

The practical guidance covered in wine cellar management tips aligns closely with what insurers expect: meticulous records, well-maintained storage, and a structured approach to collection growth. Treating your cellar as the serious investment it is means applying the same discipline to its protection.

Pro Tip: Set a calendar reminder twice yearly to cross-reference your cellar inventory against your insurance schedule. This simple habit catches discrepancies before they become claim-time problems.

Why proactive insurance is the smartest investment in your wine cellar's future

Here is the perspective that many guides miss entirely. Most collectors approach wine insurance reactively, prompted by an incident, an estate planning conversation, or a passing mention from their financial adviser. This is understandable. It is also deeply expensive as a strategy.

The surge in fine wine values over recent years has outpaced the insurance practices of the majority of collectors. 50% of wine collectors remain uninsured despite the documented surge in claims value, meaning a significant portion of the market is carrying risk they cannot absorb privately.

Standard home policies create the illusion of coverage while leaving collectors exposed to losses that would be catastrophic by any measure. A power outage lasting 48 hours in a Sydney summer can render an entire cellar undrinkable. A single burglary can erase decades of curated acquisitions. The bottles themselves cannot be replaced at purchase price once they are gone. Only agreed value, specialist coverage can make a collector whole after such a loss.

What Cellared's experience with high net worth clients across Australia and APAC consistently reveals is that the collectors who suffer most after a loss are not those who were unaware of wine insurance. They are those who assumed their existing arrangements were adequate without verifying the detail. A scheduled policy with expert insurance perspective behind it is not merely a financial instrument. It is the stewardship document that honours the care, knowledge, and investment you have put into building your collection.

The fine wine market in Australia and APAC is maturing rapidly. Trophy producers from Burgundy, Barossa, and beyond now command auction prices that would have seemed extraordinary a decade ago. A collection assembled thoughtfully over ten years may be worth three times its original cost. Without proactive, specialised insurance reviewed annually, that appreciation exists on paper alone.

Protect your investment with expert wine cellar insurance and valuation services

Knowing how to insure a wine cellar is one thing. Having the right professional partners to make it happen is quite another.

At Cellared Fine Wine, we provide court-ready, independent wine valuations that give underwriters exactly the documentation they require, and give you the confidence that your insured values reflect the true market. Our professional wine appraisals and valuations are conducted by specialists with deep market knowledge across Australian, Burgundian, Bordeaux, and broader APAC wine categories. Paired with our bespoke wine cellar management services, we help collectors maintain the storage standards and documentation trails that insurers require and that protect your claim from the moment something goes wrong.

Frequently asked questions

Does standard homeowners insurance cover my wine cellar?

Standard homeowners insurance often excludes or severely limits wine coverage, typically offering only a sub-limit of $1,000 to $2,500 that is wholly insufficient for a collection of any meaningful value.

What is the difference between blanket and scheduled wine cellar insurance?

Blanket coverage insures the entire collection with per-bottle limits applied, while scheduled coverage itemises bottles individually and removes per-bottle caps, offering superior protection for high-value or rare wines.

How often should I update my wine cellar insurance policy?

You should review and update your policy at minimum annually, and immediately after significant acquisitions, to ensure coverage reflects your collection's current insured value.

What storage conditions do insurers require for wine cellar coverage?

Insurers require climate-controlled storage at approximately 13°C and 65 to 75% humidity, with documented backup power and security systems in place to prevent spoilage and avoid grounds for claim denial.

Why is agreed value insurance important for wine collections?

Agreed value policies lock in a predetermined payout amount at the time of policy inception, eliminating disputes over market fluctuations at claim time, which is essential given the volatility inherent in fine wine valuations.