Fine wine occupies a remarkable position in the landscape of high-value assets. It ages gracefully, grows scarcer with time, and carries an almost unrivalled combination of cultural prestige and financial substance. Yet despite these qualities, many collectors across Australia and the broader APAC region remain genuinely underprepared when it comes to formally valuing what sits in their cellars. The fine wine global market reached €30 billion in 2024, driven by scarcity and historically low correlation with equities, yet the gap between a collection's actual worth and its insured value is, for too many collectors, uncomfortably wide.

Table of Contents

- The hidden risks of underinsured wine collections

- Agreed value vs. market value: Why professional appraisals matter

- Wine as a passion asset: Investment performance and total cost

- Expert valuation: Navigating edge cases and maintaining value

- What most collectors miss about wine valuation

- Professional wine valuation services for collectors

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Update valuations regularly | Reappraise your wine collection every one to three years to ensure accurate insurance and investment coverage. |

| Choose agreed value policies | Agreed value insurance protects against underinsurance and guarantees payout aligned with professional appraisals. |

| Factor in total ownership costs | Accounting for storage, insurance, and condition maintenance is essential to preserve and maximise collection value. |

| Expert advice for edge cases | Qualified appraisers address issues with ageing, provenance, and can recommend recorking clinics for optimal asset preservation. |

The hidden risks of underinsured wine collections

Consider what it means to hold a cellar assembled over two decades, bottle by patient bottle. Penfolds Grange, Giacomo Conterno Barolo, Domaine de la Romanée-Conti. These are not merely consumables. They are expressions of terroir, craftsmanship, and time, and their market values shift with the global auction landscape in ways that are rarely predictable.

The difficulty is that insurance policies, once set, tend to stay set. A policy arranged five years ago likely reflects the values of five years ago. Meanwhile, the secondary market for fine wine has moved considerably in many categories, and a single catastrophic event such as cellar flooding, fire, or theft can expose a collector to losses that no amount of personal wealth fully absorbs without the right protection in place.

High net worth individuals who hold fine wine correctly recognise that adequate insurance coverage must evolve as collections appreciate. The most common exposures include:

- Outdated declared values: A Bordeaux First Growth purchased at $400 per bottle may now trade at $1,200. Without an updated valuation, the gap between payout and replacement cost is substantial.

- Generic home and contents policies: These are rarely structured to address the unique storage, provenance, and condition requirements of fine wine, leaving collectors dangerously exposed.

- Loss without documentation: In the event of a claim, insurers require substantiated evidence of value. Collections without recent appraisals and provenance records face lengthy, contested settlements.

- Gradual spoilage: Temperature fluctuation or cork failure does not attract the same urgency as fire, yet the cumulative losses can be equally significant and are equally underinsured.

"The question is not whether to insure a serious wine collection, but whether the coverage you hold today reflects the collection you actually own today."

Specialist coverage matters here. Insuring fine wine is a distinct discipline from standard luxury asset insurance, and the nuances around agreed values, storage conditions, and provenance documentation require a partner who understands these particularities. Using the wine valuation checklist as a starting point for your review is a practical first step toward quantifying exactly where your exposure lies.

Agreed value vs. market value: Why professional appraisals matter

Not all insurance policies are created equal, and the distinction between agreed value and market value coverage is one that every serious collector should understand before a claim is ever needed.

Market value policies pay out what the insurer determines the wine to be worth at the time of loss. This sounds reasonable in principle, but in practice it can be a source of significant dispute. Wine markets are opaque, volatile in niche categories, and highly dependent on provenance and condition. A market value settlement is, by its nature, a negotiation.

Agreed value policies, by contrast, lock in a specific insured amount at the time of policy inception, based on a professional appraisal. There is no negotiation at claim time. The agreed value approach is the preferred structure for serious collectors, as it removes ambiguity and ensures that a settled, documented figure governs any payout.

The following comparison illustrates the key structural differences:

| Feature | Agreed value policy | Market value policy |

|---|---|---|

| Payout at claim | Pre-agreed fixed sum | Insurer's current assessment |

| Certainty for collector | High | Low to moderate |

| Appraisal requirement | Mandatory, periodic | Often optional or informal |

| Risk of shortfall | Minimal if updated | Moderate to high |

| Dispute potential | Low | Higher |

To maintain the integrity of an agreed value policy, professional wine valuations must be kept current. The recommended cadence for updating appraisals is as follows:

- Every one to three years for actively traded categories such as Bordeaux First Growths, Burgundy Grand Cru, and top Barossa reds.

- After any significant acquisition that materially changes the composition or value profile of the collection.

- Following major market events such as a notable auction result, a producer's release adjustment, or a critical shift in a wine's drinking window.

- Prior to any planned sale, estate transfer, or family law proceeding where an independent, court-ready appraisal may be required.

Pro Tip: Keep a dedicated provenance file for each significant wine in your collection, including original purchase receipts, storage records, and any transfer documentation. This evidence dramatically accelerates the appraisal process and strengthens any subsequent insurance or legal claim.

Wine as a passion asset: Investment performance and total cost

Fine wine exists in a fascinating space between passion and portfolio. It is consumed, yet it appreciates. It is enjoyed, yet it demands stewardship. For collectors who treat their cellars as investment assets, understanding the performance profile is essential context for making sound acquisition and valuation decisions.

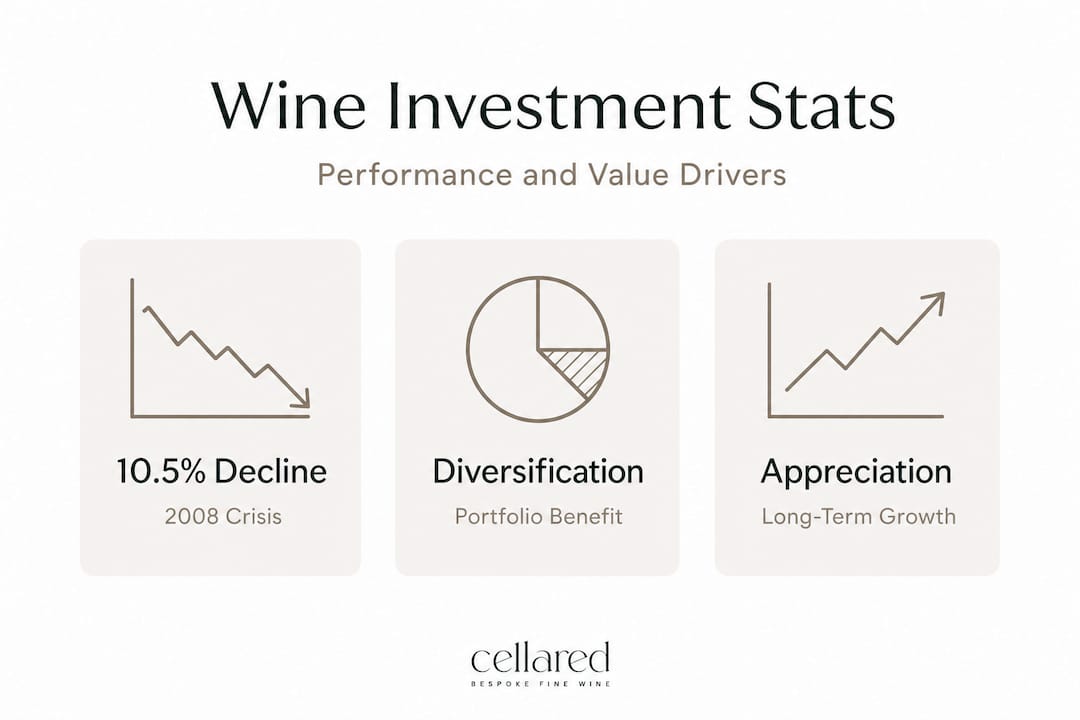

The performance data is genuinely compelling. During the 2008 global financial crisis, the Liv-ex 1000 declined 10.5% compared to the S&P 500's devastating 42.7% fall. This low correlation to equities is not accidental. Fine wine is driven by scarcity, and scarcity does not respond to central bank policy or quarterly earnings results. A great vintage of Penfolds Grange does not become less scarce because markets are volatile.

| Asset class | 2008 peak-to-trough decline | Correlation to equities |

|---|---|---|

| Fine wine (Liv-ex 1000) | -10.5% | Low |

| S&P 500 | -42.7% | High |

| Gold | -30% | Moderate |

| Global real estate | -20% to -40% | Moderate to high |

The factors that make collectible wines appreciating assets include:

- Finite supply: Once a vintage is bottled, that supply only decreases as bottles are consumed. This structural scarcity is the engine of long-term appreciation.

- Time horizon: The sweet spot for fine wine appreciation typically spans eight to twelve years. Patience is not merely a virtue here; it is a prerequisite for realising the full investment thesis.

- Producer reputation: Bottles from producers with globally recognised reputations, such as Penfolds, Giacomo Conterno, or Domaine Leroy, command consistent premiums driven by brand prestige and critical acclaim.

- Critical scores and drinking windows: Wines that receive exceptional critical acclaim often see immediate price appreciation, while those approaching optimal drinking windows attract buyer interest on the secondary market.

Yet wine investment carries real costs that are frequently underestimated at the point of acquisition. A sound fine wine portfolio strategy must account for the total cost of ownership, which includes professional-grade storage (temperature, humidity, and vibration controlled), insurance premiums, periodic appraisal fees, and the management costs associated with maintaining a collection in optimal condition.

Pro Tip: When calculating investment return expectations for fine wine, deduct total ownership costs including storage, insurance, and appraisal fees before arriving at your net return figure. Many collectors are surprised by how these costs compound over a ten-year holding period, though the result for well-chosen wines remains favourable. Understanding the full economics in advance is the hallmark of a sophisticated private wine collector.

Expert valuation: Navigating edge cases and maintaining value

Not every bottle in a mature collection has a clear, uncomplicated story. Provenance gaps, uncertain storage histories, ageing corks, and evolving drinking windows all introduce complexity into the appraisal process, and this is precisely where expert guidance becomes indispensable.

When provenance is unclear or storage conditions are in question, professional appraisers adopt a conservative approach. This is not a penalty; it is a reflection of the market reality that buyers and insurers apply similar conservatism when provenance cannot be substantiated. A single questionable link in the custody chain of a high-value bottle can reduce its achievable price by twenty to forty per cent on the secondary market.

Key scenarios that require specialist handling include:

- Inherited collections: Wines transferred through estates often have incomplete purchase histories, mixed storage conditions, and labels that require expert authentication. A professional valuation distinguishes between bottles with clear resale potential and those whose value is primarily personal.

- Ageing corks and fill levels: For older vintages, cork condition and ullage (the space between the cork and the wine) are critical valuation factors. A wine with a high shoulder fill and a compromised cork is a fundamentally different asset from the same wine in pristine condition.

- International transfers: Wines transported across jurisdictions accumulate risk. Temperature fluctuations during transit, differing storage standards, and documentation requirements all affect both condition and valuation.

- Recorking clinics: For aged Australian wines such as Penfolds Grange, recorking clinics exist to assess ongoing viability and, where appropriate, restore the bottle's sealed integrity. These clinics provide critical assurance for collectors holding older vintages and can meaningfully preserve or restore assessed value.

"The difference between a conservatively valued bottle and a properly documented, expertly assessed one is not merely academic. It is the difference between a collection that is managed and one that is merely stored."

Proper wine cellar management is, at its core, a commitment to protecting the conditions under which value is created and maintained. And for edge cases involving older vintages or uncertain provenance, specialist recorking clinics and expert assessment provide the kind of clarity that neither a spreadsheet nor a generic insurance policy can offer.

What most collectors miss about wine valuation

Here is the perspective that most discussions of fine wine valuation fail to acknowledge honestly: valuation is not primarily about liquidity. It is about stewardship, legacy, and the clarity to enjoy exceptional wine with full knowledge of what you hold.

Many collectors approach appraisals reactively, prompted by insurance renewals or estate events, rather than treating valuation as an ongoing discipline. The result is a perpetual lag between collection reality and documentation reality. This lag is where financial risk accumulates quietly, and where legal disputes, such as those arising in family law or estate proceedings, find fertile ground.

The challenge of valuing passion assets is that they generate no yield. There are no quarterly dividends, no rental income, no coupon payments. The return is entirely in appreciation and enjoyment, both of which require patience across an eight-to-twelve-year horizon and a total cost framework that most collectors only fully internalise after their first significant disappointment.

What professional stewardship actually provides, and what most collectors undervalue until they experience it, is peace of mind. Knowing precisely what your collection is worth, backed by documentation that would withstand scrutiny in a court, in an insurer's office, or across a family settlement table, transforms a cellar from a source of ambient anxiety into a genuine, manageable asset.

Sound wine cellar management tips consistently point to the same truth: the collectors who derive the greatest long-term value, both financial and personal, from their cellars are those who treat valuation, management, and enjoyment as integrated disciplines rather than separate, occasional concerns.

The contrarian insight, then, is this. Do not wait for a triggering event. Do not let the value of what you have built sit undocumented in a climate-controlled room. The wines deserve better than that, and so does the investment of time, taste, and capital they represent.

Professional wine valuation services for collectors

For collectors who are ready to move from awareness to action, Cellared Fine Wine provides the structured expertise that transforms a well-stocked cellar into a properly managed, accurately valued asset.

Whether you require an independent wine appraisals and valuations report for insurance purposes, a court-ready assessment for estate or family law proceedings, or a professional wine valuations service tailored to your broader investment strategy, Cellared brings deep market knowledge and a highly personalised approach to every engagement. For collectors seeking ongoing peace of mind, our wine cellar management service provides active stewardship of your collection, ensuring that storage, documentation, and valuations remain aligned with the true market value of what you hold. Reach out to begin a conversation about your collection.

Frequently asked questions

How often should I revalue my wine collection for insurance?

Industry experts recommend updating appraisals every one to three years to reflect market appreciation and any significant acquisitions that have altered the collection's composition or value.

What factors influence the value of a wine collection?

Scarcity, provenance, storage history, condition, and producer reputation all influence assessed value, with fine wine appreciation driven primarily by structural scarcity and low correlation to mainstream financial markets.

Can wine collections be used in investment portfolios?

Yes. Fine wine is increasingly recognised as a passion asset with genuine diversification benefits, given its historically lower volatility compared to equities, with the Liv-ex 1000 declining only 10.5% during the 2008 crisis versus 42.7% for the S&P 500.

What happens if provenance or storage is uncertain?

Collections with unclear provenance or storage history receive conservative valuations by default, though specialist recorking clinics and expert assessment can help restore confidence and documented value for older vintages like Penfolds Grange.