Fine wine is a legally recognised asset class that offers high net worth individuals and financial advisors a structured pathway to tax deferral, wealth preservation, and investment diversification. The role of wine in tax planning extends well beyond cellar aesthetics. Across jurisdictions including the UK, US, and Australia, fine wine attracts distinct tax classifications that can reduce capital gains exposure, defer duty obligations, and facilitate multi-generational wealth transfer. For APAC investors managing complex portfolios in 2026, understanding how wine intersects with tax law is not optional. It is a mark of sophisticated stewardship.

How is fine wine classified for tax purposes?

Fine wine is classified differently depending on jurisdiction, and that classification determines everything from capital gains liability to inheritance treatment. In the UK, fine wine qualifies as a wasting asset because its predictable useful life falls below 50 years. That classification exempts it from capital gains tax entirely, regardless of the size of the gain or how long the asset was held. For a collector who acquired a case of 2005 Pétrus at release and sold it decades later at a significant premium, the UK wasting asset exemption is a material financial advantage.

The United States takes a markedly different approach. Wine is treated as a collectible under US federal tax law, attracting a maximum long-term capital gains rate of 28%. That rate is higher than the 15–20% rate applied to most capital assets, which means American investors must factor in a heavier tax burden when realising gains on fine wine. The contrast with the UK exemption is stark and underscores why jurisdiction matters profoundly when structuring a wine investment portfolio.

How wine tax treatment compares across key markets

| Jurisdiction | Tax classification | Capital gains treatment |

|---|---|---|

| United Kingdom | Wasting asset (life under 50 years) | Exempt from capital gains tax |

| United States | Collectible | Up to 28% federal long-term rate |

| Australia | Capital asset (general CGT rules) | 50% discount if held over 12 months |

| France | Moveable property | Flat tax or progressive rate applies |

For APAC investors with diversified portfolios spanning multiple jurisdictions, the tax implications of wine purchases require careful legal advice. Australian residents holding fine wine as an investment asset are subject to the general capital gains tax regime, with the 50% discount available for assets held longer than 12 months. That discount makes long-term cellaring financially compelling beyond its obvious aesthetic rewards.

Pro Tip: If you hold wine across multiple jurisdictions, document the domicile of each parcel clearly from the point of acquisition. Tax residency and the location of the asset at the time of disposal can both influence which country's rules apply.

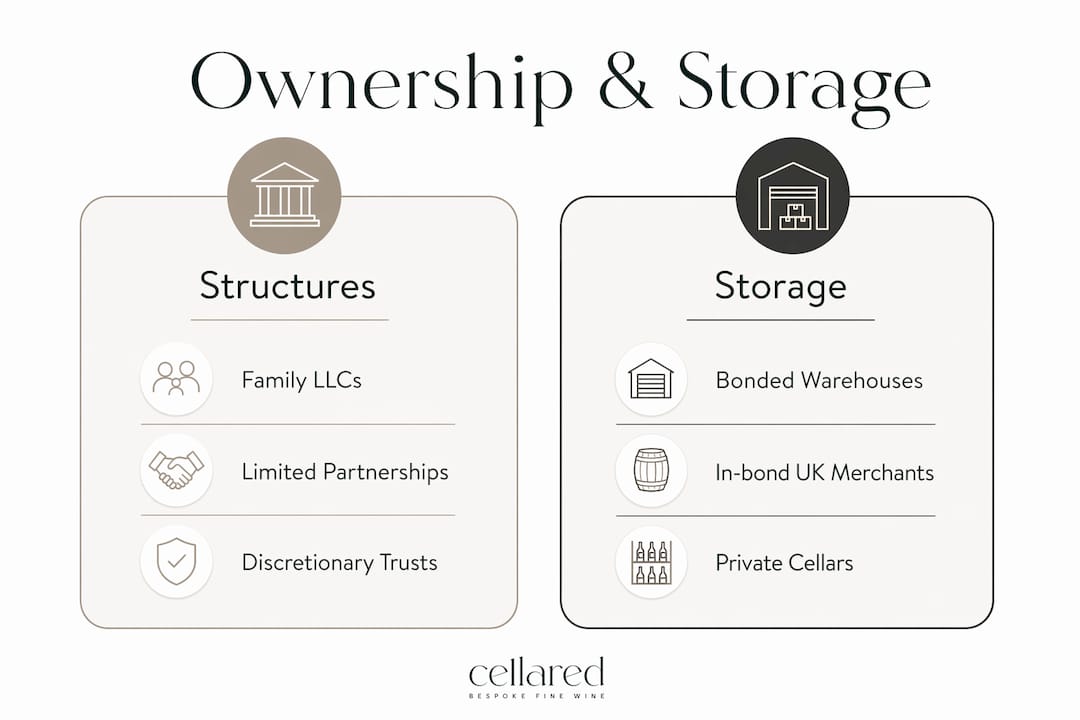

What ownership structures and storage options optimise wine tax advantages?

Entity ownership and bonded storage are among the most overlooked strategies by high net worth individuals investing in fine wine, yet they are critical for maximising tax benefits and inheritance planning. Structuring a wine collection through a family limited liability company or a limited partnership creates a legal separation between the collector and the asset. That separation allows for partial disposals over multiple years, spreading tax events rather than triggering a single large liability at the point of sale or death.

Family LLCs and limited partnerships also facilitate smoother inheritance transfers and multi-generational planning. A collection held personally passes through the estate at full value, potentially attracting significant estate or inheritance tax. The same collection held within a specialised entity can be transferred progressively, with interests gifted or sold at discounted valuations that reflect minority interest and lack of marketability. For APAC family offices managing collections worth millions of dollars, this structural distinction is not a technicality. It is a wealth preservation decision.

Storage strategy carries equal weight. Wine stored in HMRC-approved bonded warehouses in the UK attracts no VAT or duty until it is removed for personal use or sale. That deferral can extend indefinitely, preserving capital that would otherwise be consumed by tax obligations. For long-term investors, the compounding effect of retaining that capital within the collection is substantial.

Key considerations for storage and ownership planning

- Distinguish early. Identifying 'in bond' versus 'out of bond' status at the point of purchase is critical. Once wine is removed from bond, VAT and duty become immediately payable and cannot be reversed.

- Use partial disposals strategically. Selling portions of a collection across multiple tax years spreads the capital gain and keeps annual income within lower tax brackets.

- Match entity structure to succession goals. A family LLC suits multi-generational transfer. An S Corporation structure may suit a wine business owner seeking to reduce self-employment tax obligations, with potential annual FICA savings of $8,000 to $15,000 once net profit exceeds $80,000–$100,000.

- Document provenance and storage history. Tax authorities require clear evidence of asset classification, storage conditions, and acquisition costs. Gaps in documentation create audit exposure.

Pro Tip: For Australian investors purchasing fine wine through UK merchants, request that bottles remain in bond at a London City Bond or Octavian facility. The VAT and duty deferral applies regardless of your tax residency, preserving cash flow until you decide to ship or sell.

What are the common challenges in wine tax planning for businesses and collectors?

Wine businesses and serious collectors face a layer of tax complexity that personal investors in equities or property rarely encounter. The Uniform Capitalisation rules, known as UNICAP, require wineries to capitalise both direct and indirect costs into inventory rather than expensing them immediately. Direct costs include grapes, barrels, and labour. Indirect costs include rent, utilities, and depreciation allocated to the production process. Failing to apply UNICAP correctly distorts gross margins and creates significant audit risk.

The timing of cost recognition is equally consequential. Costs capitalised into inventory do not reduce taxable income until the wine is sold. A winery that bottles a vintage in one financial year but sells it two years later carries those costs on the balance sheet throughout. Precise monthly allocation of indirect costs under UNICAP is critical to avoid audit failures and to ensure deductions are claimed in the correct period.

A practical framework for wine business tax compliance

- Separate inventory from operating costs. Production costs attach to inventory under UNICAP. Administrative and selling costs are expensed as incurred. Mixing these categories is the most common audit trigger for wine businesses.

- Align equipment purchases with tax cycles. Accelerating qualifying equipment deductions and timing them to offset peak revenue years reduces overall tax liability materially.

- Plan vintage releases around tax deferral. Holding a release until the following financial year defers the associated revenue recognition, smoothing taxable income across periods.

- Review depreciation schedules annually. Barrels, tanks, and cellar equipment depreciate at different rates. Reviewing these schedules before year end identifies opportunities to accelerate deductions.

| Tax challenge | Risk if unmanaged | Best practice |

|---|---|---|

| UNICAP non-compliance | Audit, restated margins | Monthly indirect cost allocation |

| Premature cost expensing | Overstated deductions | Capitalise until point of sale |

| Poor vintage release timing | Compressed taxable income | Multi-year release scheduling |

| Undocumented storage status | VAT/duty liability triggered | Maintain bonded warehouse records |

Year-round tax planning that coordinates vintage releases with tax deferral and cash flow strategy is the discipline that separates well-structured wine businesses from those that scramble at year end. The most effective operators treat tax planning as an operational function, not an annual compliance exercise.

How does wine investment integrate with estate and wealth planning?

Luxury tax planning for high net worth individuals is proactive, involving multi-year asset structuring and coordination across asset classes to preserve wealth and minimise redundant costs. Fine wine fits naturally within this framework because its value appreciates over time, its liquidity can be managed through selective disposal, and its physical nature lends itself to trust and entity structures that other asset classes do not accommodate as elegantly.

Estate planning with fine wine requires particular attention to valuation. An estate that includes a significant wine collection must present an accurate, defensible valuation for probate purposes. Undervaluing a collection to reduce estate tax exposure is a compliance risk. Overvaluing it inflates the tax burden unnecessarily. Independent, market-led valuations from specialists like Cellared Fine Wine provide the documentation that tax authorities and legal advisors require. You can explore the legal aspects of wine collections in detail to understand how ownership and valuation intersect with estate law in Australia.

- Use trusts for long-term preservation. A discretionary trust holding a fine wine collection allows the trustee to distribute assets or income to beneficiaries across multiple years, managing tax exposure at the beneficiary level.

- Coordinate wine with art and real estate. Multi-asset structuring across collectibles, property, and alternative investments creates a more tax-efficient overall portfolio than managing each asset class in isolation.

- Plan for succession early. Transferring interests in a wine-holding entity to the next generation while values are lower reduces the taxable transfer. Waiting until the collection has appreciated significantly narrows the planning options.

- Review collection exit strategies. Whether the goal is auction, private sale, or gifting, each wine collection exit strategy carries distinct tax consequences that should be modelled before a decision is made.

For APAC financial advisors, the practical guidance is clear. Fine wine is not a peripheral asset to be addressed after the core portfolio is structured. It belongs in the same conversation as real estate, private equity, and art, with the same rigour applied to ownership structure, valuation, and succession planning.

Key takeaways

Fine wine is a tax-efficient asset when held within the right structure, stored correctly, and integrated into a proactive multi-year wealth plan.

| Point | Details |

|---|---|

| Jurisdiction shapes tax treatment | UK wasting asset exemption eliminates CGT; US collectible rate reaches 28%; Australia applies the 50% CGT discount for assets held over 12 months. |

| Bonded storage defers tax obligations | Wine held in approved bonded warehouses attracts no VAT or duty until removed, preserving capital for long-term investors. |

| Entity ownership aids succession | Family LLCs and limited partnerships allow partial disposals and progressive transfers, reducing estate tax exposure across generations. |

| UNICAP compliance is non-negotiable | Wine businesses must capitalise direct and indirect production costs into inventory or face audit risk and distorted margins. |

| Valuation accuracy protects estates | Independent, market-led valuations are required for probate, insurance, and tax reporting to avoid compliance risk. |

Why most wine investors leave tax advantages on the table

I have worked with collectors and advisors across Australia and the broader APAC region for long enough to recognise a consistent pattern. The majority of high net worth individuals who own significant wine collections have never had a structured conversation about how that collection is held, where it is stored, or what happens to it when they die. They have thought carefully about what they buy. They have not thought carefully about the structure around what they own.

The bonded storage question is the most glaring missed opportunity I encounter. Investors who have spent years acquiring exceptional Burgundy or aged Barolo from the Langhe will store it domestically, pay the duty upfront, and never recover that tax efficiency. The same collection held in bond would have preserved that capital indefinitely. The difference over a decade of compounding is not trivial.

The second pattern is the absence of entity structure. A collection worth $500,000 held personally is an estate liability at full value. The same collection held within a family trust or limited partnership is a transferable interest that can be gifted progressively, valued at a discount, and passed to the next generation with far less friction. These are not exotic strategies. They are the standard tools of sophisticated wealth management applied to an asset class that deserves the same rigour as property or private equity.

My honest view is that fine wine rewards patience twice. Once in the glass, and once in the structure around it.

— David

How Cellared Fine Wine supports your tax and investment planning

Cellared Fine Wine works with collectors, investors, and estates across Australia and APAC to provide the documentation, structure, and market knowledge that serious wine tax planning demands. From court-ready wine valuations prepared for probate, insurance, and family law purposes, to bespoke cellar management services that maintain bonded storage status and collection integrity, Cellared brings the depth of expertise that financial advisors and their clients require. If your collection is a meaningful part of your wealth, it deserves the same professional attention as any other asset on your balance sheet. Speak with the team at Cellared Fine Wine to understand how your collection can be structured, valued, and managed with greater clarity and confidence.

FAQ

Is fine wine exempt from capital gains tax in Australia?

Fine wine held as an investment in Australia is subject to the general capital gains tax regime. Investors who hold wine for more than 12 months qualify for the 50% CGT discount, reducing the effective tax rate on any gain.

What is the wasting asset exemption and does it apply in Australia?

The wasting asset exemption is a UK tax rule that exempts chattels with a predictable useful life of under 50 years from capital gains tax. This exemption does not apply in Australia, where wine is treated as a standard capital asset under the Income Tax Assessment Act.

How does bonded storage reduce tax liability for wine investors?

Wine stored in an HMRC-approved bonded warehouse in the UK attracts no VAT or duty until it is removed for personal use or sale, deferring those obligations indefinitely and preserving capital within the collection.

Can a family trust hold a fine wine collection for estate planning purposes?

A discretionary trust can hold a fine wine collection, allowing the trustee to distribute assets or income to beneficiaries across multiple years and manage tax exposure at the beneficiary level. This structure also facilitates progressive transfer to the next generation.

What documentation does the Australian Taxation Office require for wine as an investment asset?

The ATO requires clear records of acquisition cost, date of purchase, storage history, and sale proceeds for any capital asset including fine wine. Independent valuations from qualified specialists support accurate reporting and reduce audit exposure.