Global wine consumption has reached its lowest point since 1957, yet fine wine prices in key segments continue to rise. For collectors and investors, this apparent contradiction sits at the heart of understanding wine market trends today. The market is not simply contracting or expanding. It is restructuring, with volume softness masking genuine value growth in premium tiers, and emerging categories rewriting demand patterns that held firm for decades. Reading the market accurately, rather than reacting to headlines, has never mattered more for those making serious acquisition, valuation, or portfolio decisions.

Table of Contents

- Key takeaways

- Understanding wine market trends: the global picture

- When falling volumes and rising values coexist

- Price tiers and segments: where the divergence is sharpest

- Fine wine stabilisation: reading the recovery signals

- How to analyse wine market data for real decisions

- My perspective on what the market is telling us right now

- Navigate the market with Cellared Fine Wine

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Volume decline does not equal value collapse | Global consumption is falling, but premium wine segments are holding and growing in value simultaneously. |

| Segmentation is everything | Sub-$5 wines are haemorrhaging volume while wine-based RTD and non-alcoholic categories grow strongly. |

| Fine wine is stabilising | Prices have risen for six consecutive months but remain well below 2022 peaks, creating measured opportunity. |

| Channel data reveals true market health | Direct-to-consumer shipment declines expose brand weakness that headline price data can obscure. |

| Data-driven strategy outperforms intuition | Tracking multiple price tiers and channels is the foundation of sound valuation and acquisition decisions. |

Understanding wine market trends: the global picture

To properly grasp what is happening across the global wine market, you must first confront a structural reality that no amount of vintage optimism can wish away. Global consumption fell 2.7% in 2025 to 208 million hectolitres, a level not seen since 1957. This is not a single-year anomaly. Consumption has dropped by a cumulative 14% since 2018, driven by a convergence of economic strain, shifting health preferences, and profound demographic change.

The major consuming markets tell a consistent story. The United States, France, and China have all recorded meaningful volume declines. In China, the retreat from wine has been particularly sharp, reflecting both economic headwinds and a pivot toward domestic spirits among younger consumers. In France, structural changes in drinking culture are reshaping a market once considered the bedrock of global demand.

| Market | Trend direction | Primary driver |

|---|---|---|

| United States | Volume declining, value rising | Premiumisation, fewer but higher-spend occasions |

| France | Volume declining | Cultural shift, moderation movement |

| China | Volume declining sharply | Economic caution, preference for domestic spirits |

| Global fine wine | Stabilising and recovering | Fundamentals-driven demand return |

The OIV underlines that structural shifts underpin this decline, placing it beyond the reach of a single good harvest or marketing campaign to reverse. For collectors and investors, this context is not discouraging. It is clarifying. A smaller market that concentrates value in premium tiers is, in many respects, a more favourable environment for serious fine wine investment than an indiscriminate bull run that inflates everything equally.

When falling volumes and rising values coexist

The US wine market in 2025 offered one of the clearest illustrations of how explaining market trends in wine requires more than a single metric. Overall volume fell, yet market value rose 3%, driven by higher prices and a premiumisation effect that pushed consumers toward fewer, more expensive bottles.

This divergence is not unique to the US. It reflects a broader structural reset: consumers who continue to drink wine are spending more per bottle, while casual, everyday drinkers are leaving the category or migrating toward alternatives. The result is a market that looks healthier in revenue terms than it actually is from a volume and distribution health perspective.

Channel data makes this tension visible in ways that aggregate figures do not. Direct-to-consumer shipments fell 15% in volume and 6% in value in the US in 2025. For premium wineries that depend on DTC sales for both cash flow and brand relationship, this is a material warning sign. A winery posting a higher average bottle price while losing DTC momentum may be concealing deeper demand erosion behind a flattering headline.

BMO's analysis reconciles value growth with volume declines as the key to truly understanding industry health. For anyone assessing a cellar, building a portfolio, or commissioning a valuation, this is the methodology worth adopting.

Pro Tip: When reviewing market reports, always cross-reference headline value figures with channel-specific data such as DTC performance and distributor sell-through rates. A rising average price without corresponding volume strength can signal brand fragility rather than genuine demand growth.

Price tiers and segments: where the divergence is sharpest

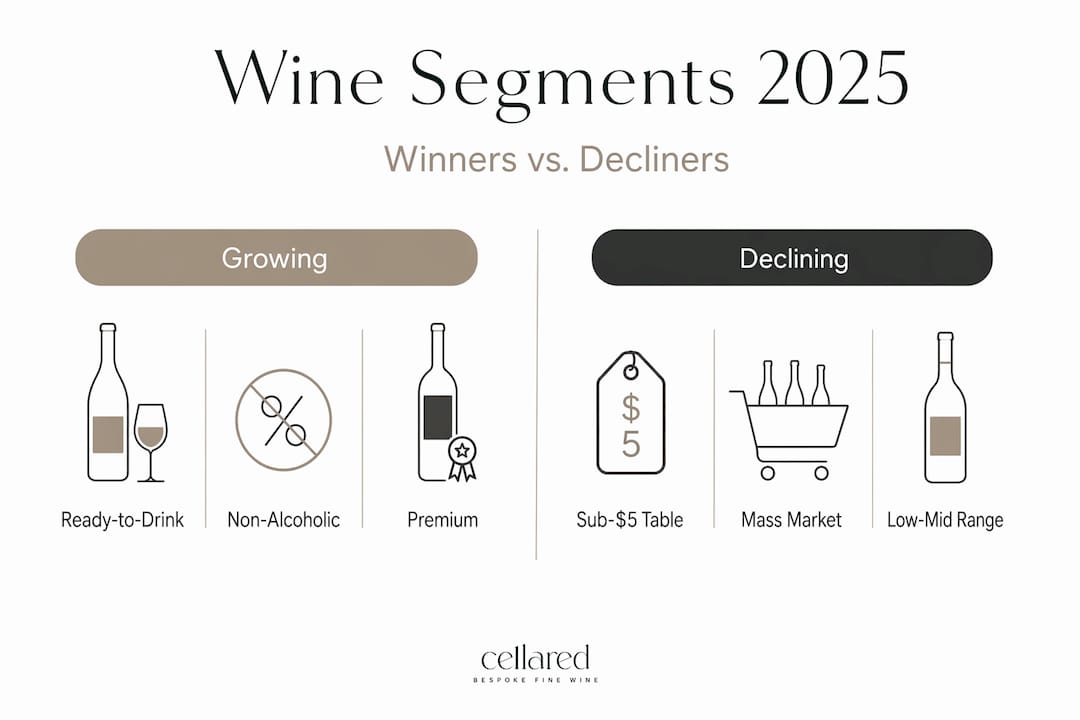

Not all wine is experiencing the same market conditions, and this is where the analysis becomes genuinely useful for collectors and investors. The sub-$5.00 segment saw volume collapse by 19.1% in Q1 2026 according to SipSource data, while overall US wine market volume dropped 8.3% and revenue fell 5.3%. This is a market shedding its most price-sensitive consumers at pace.

Meanwhile, two categories are defying the broader contraction. Wine-based ready-to-drink beverages grew 30% in 2025, and non-alcoholic wines expanded 22%. These are not marginal curiosities. They represent a structural shift in how younger consumers engage with wine culture, often prioritising occasion and convenience over tradition.

The comparison below captures what is driving divergence across price tiers:

| Segment | 2025 performance | Key driver |

|---|---|---|

| Sub-$5 table wine | Sharp volume decline | Price-sensitive consumers exiting |

| Premium and luxury wine | Resilient to growing | Affluent buyers less price sensitive |

| Wine-based RTD | +30% volume growth | Younger consumers, occasion-led purchasing |

| Non-alcoholic wine | +22% growth | Health-conscious demand |

| White and sparkling | Relative resilience | Versatility, food pairing appeal |

Terrain's analysis reinforces that premium and luxury segments are poised to outperform precisely because their buyers are structurally less exposed to economic volatility. This is not a temporary reprieve. It reflects the enduring logic of fine wine as a category defined by scarcity, terroir, and provenance, qualities that do not depreciate with shifting macroeconomic tides. Understanding this segmentation is foundational to building a rare wine portfolio with genuine long-term integrity.

Fine wine stabilisation: reading the recovery signals

For those whose interests sit squarely in the collectible and investment-grade market, the most consequential development of late 2025 and early 2026 has been the measured stabilisation of fine wine prices. Liv-ex data and Wine-Intelligence together indicate that prices have risen consecutively for six months, though they remain 25 to 30% below their 2022 peaks.

This is not a speculative recovery. The character of demand returning to the fine wine market is fundamentally different from the frenzied accumulation that defined 2021 and 2022. Several signals distinguish this phase:

-

Fundamentals are driving buying decisions. Collectors are acquiring wines with genuine drinking and cellaring merit rather than chasing momentum. Producers with strong terroir expression, consistent quality across vintages, and genuine scarcity are attracting sustained attention.

-

Diversification beyond blue-chip labels is accelerating. The fine wine market is broadening its geography and its imagination. Regions such as Champagne, Barolo, Burgundy from less-celebrated appellations, and even select New World producers are drawing sophisticated buyers who once confined themselves to first-growth Bordeaux.

-

Younger, data-driven investors are reshaping the market. This cohort approaches wine with the analytical rigour of an asset class, consulting secondary market indices, wine valuation standards, and auction records before committing capital.

-

Liquidity is selective. Not all wines are finding buyers equally. Bottles with clear provenance, appropriate storage history, and genuine demand across multiple markets move. Those without these qualities are sitting longer, regardless of appellation prestige.

Fine wine's fundamentals-driven demand signals a sustainable growth cycle rather than another speculative peak. For collectors building or rationalising a cellar, this environment rewards patience, specificity, and precise valuation over enthusiasm alone.

Pro Tip: If you are considering acquisitions in 2026, use the current 25 to 30% discount from 2022 highs as a reference point, not as a floor. Assess each wine on its own fundamentals, storage integrity, and market liquidity before treating any price point as automatically attractive.

How to analyse wine market data for real decisions

Interpreting wine market data well is a discipline, not a talent. The practitioners who navigate the role of market trends in wine investment most capably share a common methodology: they track multiple channels, resist the pull of single-metric analysis, and treat macroeconomic context as a permanent input rather than a background variable.

The most common errors among collectors and investors include:

- Over-relying on aggregate price indices. Headline indices capture blue-chip labels disproportionately. A rising Liv-ex 100 does not mean that the mid-tier Burgundy you are considering shares the same momentum.

- Ignoring channel health. Tracking multiple channels avoids misreading trends and the risk of overpaying in valuation. DTC decline in a producer's home market is a meaningful signal that no secondary market price can fully disguise.

- Treating consumption data as a proxy for collectible demand. Secondary market prices decouple from bulk consumption trends, requiring segmented analysis for accurate valuation. The fact that table wine volumes are collapsing globally is largely irrelevant to the pricing of a 2019 Barolo from a renowned single vineyard.

- Underestimating demographic shift. The ageing of core wine-consuming demographics in France, Germany, and the US is not temporary. Planning a long-term portfolio without accounting for this structural reality is a meaningful oversight.

- Valuing without independent market data. Whether you are acquiring, insuring, or settling an estate, valuations grounded purely in purchase price or catalogue estimates without reference to current market conditions carry significant risk. Commissioning professional wine appraisals based on live market data is the standard that courts, insurers, and sophisticated counterparties increasingly expect.

The most effective framework for how to estimate wine market trends in any given segment combines price tier analysis, channel health data, secondary market transaction records, and a macroeconomic overlay. None of these inputs alone tells the full story. Together, they produce a reading of the market that is genuinely useful for acquisition, disposition, and valuation decisions.

My perspective on what the market is telling us right now

I have watched market narratives simplify complexity into comfortable stories for as long as I have worked with serious collectors and investors. Right now, the dominant story is either catastrophe (global consumption collapse) or quiet optimism (prices stabilising). My experience tells me both framings miss the most important truth.

What I see in 2026 is a market engaged in a long-overdue reckoning with its own segmentation. The wine world is not one market. It never was. But the convergence of cheap money, pandemic-era exuberance, and speculative demand between 2020 and 2022 obscured the fault lines that are now fully visible. The correction was not only inevitable. It was necessary.

What I find genuinely encouraging is the character of the demand that has returned. The collectors and investors I work with today are asking harder, better questions: about provenance, about storage, about liquidity across multiple markets, about the specific vintage dynamics of what they are buying. That rigour was sometimes absent during the bull run.

The diversification trend matters enormously too. A collector who confines interest to a handful of blue-chip Bordeaux and Burgundy labels is carrying concentration risk that the current market will expose. Those broadening their aperture into Champagne, the Rhône, Barolo, and select New World appellations are building collections with both depth and resilience.

Patient, data-driven engagement with the market is not a cautious second-best strategy. It is the strategy that performs across cycles.

— David

Navigate the market with Cellared Fine Wine

The complexity of today's wine market rewards those who approach it with discipline, depth, and access to independent expertise. Whether you are acquiring with intention, managing an existing cellar, or requiring a valuation for insurance, probate, or family law purposes, having a specialist in your corner changes the quality of every decision you make.

Cellared Fine Wine offers bespoke wine services spanning professional court-ready valuations, private cellar management, and meticulous sourcing of rare and hard-to-find bottles. Every service is grounded in live market intelligence and calibrated to the realities of 2026's complex, segmented wine market. If you are looking to buy well, value accurately, or manage your collection with greater clarity, Cellared is the specialist partner built for exactly this environment.

FAQ

What is driving the decline in global wine consumption?

Consumption has fallen 14% since 2018, driven by a combination of economic pressures, health-oriented behaviour shifts, and demographic changes in core wine-drinking markets including the US, France, and China.

Can wine market value rise even when volumes are falling?

Yes. The US market demonstrated this precisely in 2025, with value growing 3% while volume declined, as premiumisation and higher per-bottle spending offset the loss of casual drinkers from the category.

How do fine wine prices compare to their 2022 peak?

Prices have risen for six consecutive months in early 2026 but remain 25 to 30% below their 2022 highs, representing a stabilised market with selective opportunity rather than a full recovery.

Which wine segments are currently growing?

Wine-based ready-to-drink beverages grew 30% and non-alcoholic wines grew 22% in 2025, while premium and luxury segments are outperforming the broader market due to the relative price insensitivity of affluent buyers.

Why is channel data important for wine valuation?

Channel-specific metrics such as DTC shipment volumes reveal brand health and underlying demand signals that aggregate price data can obscure, making them critical inputs for any accurate and defensible wine cellar valuation.